I have traded crude oil since grade nine in high school when my mom mentored me on this subject and I helped her to do market research and to execute actual crude oil trades. Over the next few years, I would start out on my own and develop my own ideas, thesis, and investing models involving knowledge across a variety of different disciplines. Throughout my ten years of crude oil trading experience, I have experienced gains and losses as well. To understand crude oil price movement, one must learn short term technical analysis. To build a general understanding of crude oil over time, subjects such as economics and politics must be learned and daily news must be read as crude oil is influenced by global supply and demand and political regulations and policies including sanctions and free trade as well as unpredictable daily events. I will layout the macroeconomic perspective followed by some of my personal findings and things I look for when investing in crude oil. In general, only invest when the upside is much greater than the downside otherwise the losses will outweigh the gains much like playing a hand of poker when you only take a chance when you have great cards with a good chance of winning.

The economic theory of storage arbitrage, crude oil futures and non-renewable crude oil depletion will be discussed. Moreover, the factors that affect crude oil prices including political, economic, supply and demand as well as geopolitical risk will be touched on.

Supply Side

OPEC controls the crude oil prices through production output changes. OPEC or the organization of the petroleum exporting nations control more than ¾ of the world’s oil reserves.1 They include twelve members consisting of Venezuela, United Arab Emirates, Saudi Arabia, Qatar, Nigeria, Libya, Kuwait, Iraq, Iran, Ecuador, Angola, and Algeria and produce about 40% of the world’s oil to meet demands.2 Historically, OPEC dictated the global crude oil prices through production level changes with oil production cuts when crude oil prices are low (approx $80USD/barrel) or increased production when crude oil prices when above $100USD/barrel. Thus crude oil historical over the past decade tends to stay within $80-100USD/barrel range.3

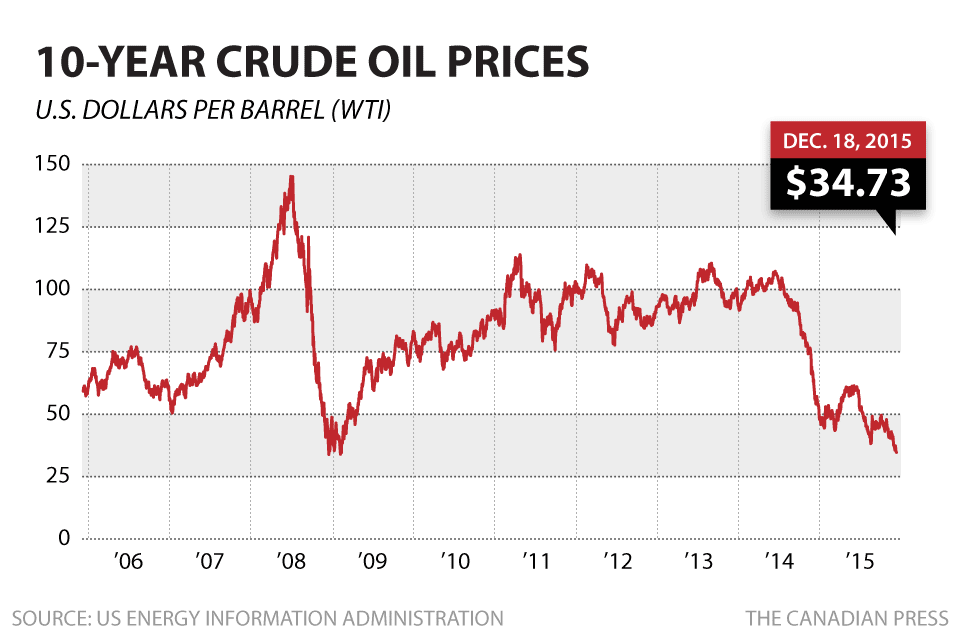

The oil shale or kerogen shale boom in the US has decreased foreign oil dependency and increased global crude oil market share for the US. In the long term, US global market share of crude oil would have continued to increase had crude oil prices remained at $100 USD/barrel due to the leveraging effects of debt that many oil companies used to finance their acquisitions and expansion of operations n order to increase profit. OPEC would have lost the effectiveness of its oil market price control ability through increases and cuts in crude oil output as it slowly lost global crude oil market share. The greatest threat to OPEC’s market share is mega projects with start up costs in the billions which can bring excess supply to the market with a production life in excess of 20-30+ years and would not be shutdown once it is operational due to positive cash flow that stems from the project. The rapid decrease in crude oil prices from $100+ in June 2014 to under $40/barrel in December 2015 meant that the risk profile of these capital intensive mega projects were negatively impacted. These executives in these large corporations will not start up the project again for decades once it is shutdown as in the case with Shell’s abandonment of Arctic exploration which no longer made economic sense given the potential crude oil price uncertainty and increased volatility.3

The reduction in geopolitical risk. As geopolitical risk increases in crude oil rich countries, the uncertainty of crude oil supply shortages increases due to the disruption in the crude oil supply chain. This has a positive effect on the increase in crude oil prices. In the first half of 2011, the civil war in Libya disrupted the crude oil supply and decreased global supply and when supply is low, the economics of supply and demand meant that prices will increase. In 2014, port blockage of crude oil transport in Libya created uncertainty by decreasing crude oil output out of Libya. Geopolitical risk, however, is short lived and causes temporary rapid changes in crude oil prices. Once the issue or problem resolves itself, crude oil prices will revert back to normal levels.

Increasing volatility caused by price speculation. Traders and speculators place bets on the underlying direction of crude oil price movement. This speculation on price exaggerates price swings. For example, if actual crude oil prices is projected to go up to only $90USD/barrel without a futures market, the price swing exaggeration might bring prices up to $105+USD/barrel with the existence of a futures market as speculators rent crude oil storage facilities to store crude oil inventory to sell later as supply tightens. This removes inventory from the market which further worsens the supply shortage causing prices to increase. Conversely, when prices are low, speculators dump crude oil futures onto the market which further dampening or decreasing the price and the price decline accelerates. Once crude oil reaches variable cost of crude oil extraction, speculators will start to store excess crude oil on tankers and crude oil storage facilities which should slow down price declines. If crude oil storage facilities reach storage capacity, and there is no new facility to store crude oil, then prices will rapidly decline as the newly extracted crude oil is sold on the open market for what the buyers are willing to pay.

Demand Side

The state of the Chinese economy affects global crude oil prices. China overtook the US as the largest economy in 2014. Being the largest economy meant that a large percentage of global demand for commodities comes from China. If the Chinese economy improves, the demand for these commodities including crude oil increases which increases global prices. In 2015, the Chinese economy has faltered due to a slowing economic growth with demand for these commodities decreasing which dampens global prices of commodities including crude oil.

Pedestrians on Nanjing Road

Seasonality – refineries

Refinery seasonality affects crude oil prices. Crude oil trades in short term and long term cycles. Annually, the crude oil price cycle is dependent on refinery demand. In January and February, crude oil prices are fairly steady as people use less of the crude oil derivatives such as gasoline for driving. This is balanced by full capacity production from refineries which use up the crude oil to make derivative products. In March and April, refineries shutdown to switch to a summer blend which causes crude oil inventory to build up and prices decrease. From May through August, the refineries are near full capacity to meet the demand for the summer driving season. This reduces the crude oil supply as refineries turn the crude oil into its derivative products and price of crude oil increases. From September to October, the refineries are shutdown and refitted with a winter blend. Crude oil prices decrease due to the increase in inventory. From November to December, crude oil prices increase as use of heating oil in homes due to winter increases due to the positive relationship of crude oil and heating oil. Heating oil is a derivative of crude oil. As heating oil is used, refineries convert more crude oil to its derivatives further decreasing the supply and causing the price to increase.

Future outlook:

We look and learn from the past to understand the future. The crude oil market has seen a rapid price decline from over $100+ USD/barrel in 2014 to a low of under $27 USD/barrel in early 2016. This rapid decline in crude oil prices is due to an increasing global crude oil production output coupled by a slowing down of the global economy led by China which dampened crude oil future demand outlook. Prices in crude oil were in free fall in 2015 and looks to stabilize in 2016 around $40-50 /barrel range. Speculatively, we can expect prices to slowly increase to $65-$70 in 2017 once crude oil production cuts are finalized with the various OPEC nations and Russia. In 2018, crude oil prices may once again touch above $80 / barrel. In 2020 to 2025, due to recent decreases in capital expenditure in bringing online new crude oil projects, crude oil prices may once again reach $100-$110 USD/barrel due to supply shortage from new supply. Once crude oil prices reach this level, many small and large oil companies will once again increase crude oil production to full capacity to capture this excess profit. It is within 1-2 years of this point, that crude oil prices may once again free fall and provide a trigger to reset the market for the cycle to begin again.

Reference:

1 http://www.opec.org/opec_web/en/data_graphs/330.htm