Overview

The logging industry harvests trees which are transported as sawlogs to pulp mills and sawmills to be processed. The industry experiences growth as well as downturns typical of cyclical industries. Currently, the industry is in a deep cyclical decline with commodity prices declining rapidly over the past year and the weakened demand from China due to slowing economic growth.

The logging industry is fragmented with no market leaders with the top four companies owning about 15% of the market (Canfor Corporation 4.9%, West Fraser Timber Company 4.6%, Resolute Forest Products Inc. 3.2%, and Western Forestry Products 2.3%).

The main activities of this industry are the cutting, and transporting of timber and wood chip production. The main products produced are hardwood bolts and logs, softwood bolts and logs, and pulpwood.

The last five years has seen demand increase from manufacturers of forestry products especially in the growing construction industry in Asia especially the housing boom in China despite a 0.6% decrease in revenue in 2015 to $10.6 billion and plummeting demand in Canadian housing. The shutdown of pulp mills due to a shift away from paper and towards a digital infrastructure has decreased demand at an annualized revenue rate of 6.9% in the last five years.

Key Drivers

The key drivers of the industry are dependent on wood product prices, Canadian dollar exchange rate and housing starts. As demand for products increases or there is a shortage of wood supply, the price of wood products go up leaving to greater revenue and profit margin. The higher the price of wood products, the greater the profit and the more money can be invested into new harvest sources. The lower the Canadian exchange rate relative to other currencies such as US dollar, the more attractive or affordable the product is to foreign buyers as the product will be cheaper in the buyer’s currency such as US dollar. As the number of housing starts increases which use wood products in its construction, the greater the demand for wood products which increases the volume sold and/or increases the price if there is a supply shortage.

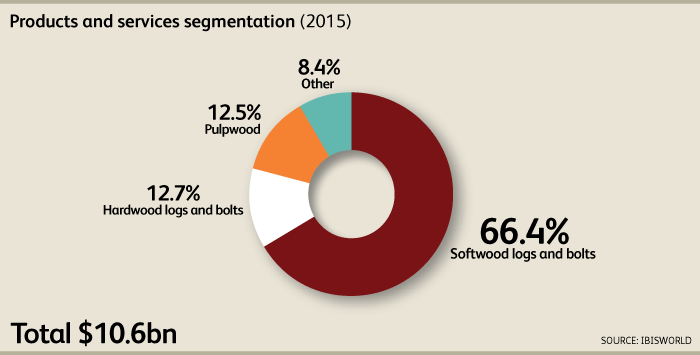

Products segmentation

The breakdown of the $10.6 billion revenue into product segments is 66.4% softwood bolts and logs used in residential construction (amabilis fir, Douglas fir, western hemlock, Jefrey pine, lodgepole pine, ponderosa pine ad black and white spruces), 12.7% hardwood bolts and logs used in construction, flooring, furniture, making instruments (maple, alder, aspen, birch, poplar), 12.5% pulpwood used in paper products production and 8.4% other as visualized below.

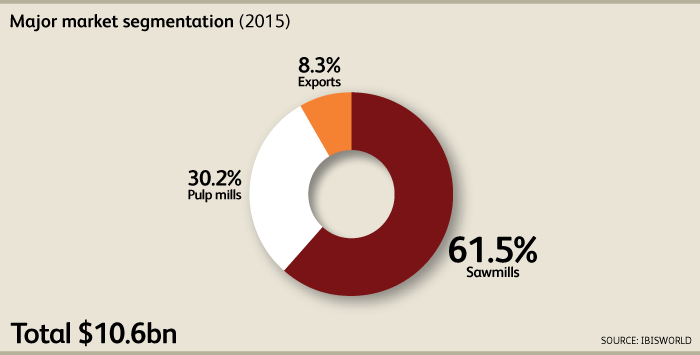

2015 Market segmentation

Sawmills purchase 61.5% of industry log production and the mills remove the log bark and cut the log beams, boards, poles, sidings, and wood chips. The finished products are sold to wholesalers who supply them to the construction industry.

Pulp mills purchase wood chips produced by logging companies make up 30.2% of the market and convert them into paper, and tissue related products.

Exports make up 8.3% of the market and global trading to China, Japan and US make up 83.9% of the export market as shown in the pie chart below.

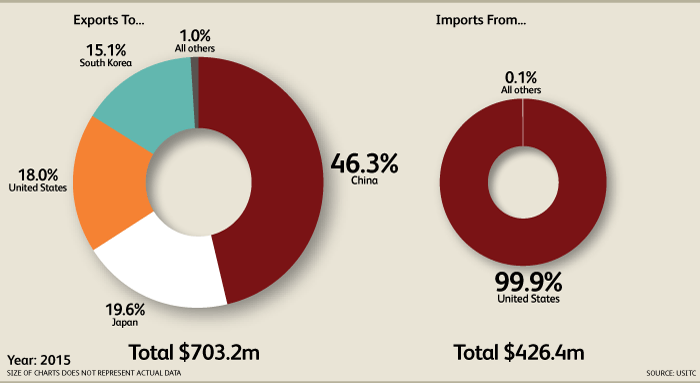

Global exports and imports in the Canadian logging industry

Of the export portion of the business, about 50% are exported to China with 80% of all exports going to Asia. Imports only make up 4.1% of domestic demand with almost all demand being met by the US.

Industry structure

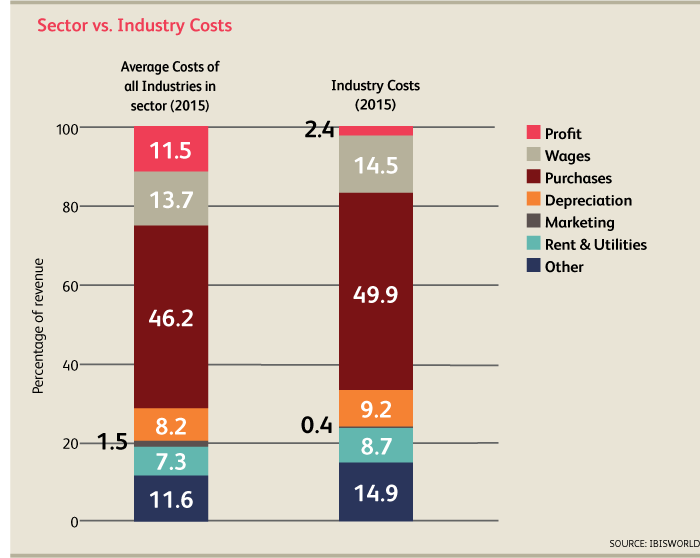

Profit: In recent years, the industry profit margin has fallen to 2.4%. For larger forestry companies with economies of scale and greater negotiating power, the profit margin is higher while smaller players without economies of scale have lower profit margins. This greatly fluctuates due to demand of wood products, wood product prices, fuel prices with high fuel costs meaning lower profits.

Wages: Wages are the second highest expense at 14.5% behind purchases due to decreases in labor cost from a lower Canadian exchange rate from paying Canadians CAD dollar, technological advancement which bring greater efficiency and less specialized labor which lowers labor costs and puts a cap on future wage increases.

Purchases: Purchases make up the greatest expense at 49.9% of revenue in the form of provincial royalties and payments for timber access to public and private land to harvest timber based on government mandated quota.

Depreciation: Depreciation makes up 9.2% of industry revenue in the form of logging equipments, tools and machineries.

Rent and utilities: Rent is fairly constant with long term signed lease contracts. Utilities cost is dependent on fuel prices in operating of machineries and log transportation vehicles.